Medicare Advantage plans in Arizona combine hospital, medical, and often prescription drug coverage into one plan offered by private insurers. Costs, provider networks, and benefits vary by county. Seniors should compare premiums, out-of-pocket maximums, drug formularies, and doctor networks annually to avoid unexpected expenses.

Medicare Advantage plans in Arizona are private insurance alternatives to Original Medicare that bundle Part A, Part B, and often Part D coverage. Costs vary by county and plan, with many offering $0 premiums but requiring copays and network use. Comparing provider access, prescription coverage, and maximum out-of-pocket limits is essential.

What Is Medicare Advantage in Arizona?

Medicare Advantage, also known as Medicare Part C, is an alternative way to receive your Medicare benefits through private insurance companies that are approved and regulated by the federal Medicare program. Instead of receiving coverage directly from Original Medicare (Part A and Part B), you enroll in a private plan that bundles your benefits into one coordinated package.

In Arizona, Medicare Advantage plans are required to provide at least the same level of coverage as:

- Medicare Part A (Hospital Insurance) – Covers inpatient hospital stays, skilled nursing facility care, hospice care, and limited home health services.

- Medicare Part B (Medical Insurance) – Covers doctor visits, outpatient care, preventive services, lab tests, durable medical equipment, and certain home health services.

This means you receive the same core protections as Original Medicare — but often with additional benefits and a different cost structure.

Additional Benefits Often Included

One of the key reasons Arizona seniors consider Medicare Advantage plans is the extra coverage many plans offer beyond Original Medicare. While benefits vary by carrier and county, most plans include:

- Medicare Part D (Prescription Drug Coverage) – Integrated drug coverage so you don’t need to purchase a separate Part D plan.

- Dental Benefits – Preventive cleanings, X-rays, and sometimes allowances for more advanced procedures.

- Vision Coverage – Eye exams and allowances for glasses or contact lenses.

- Hearing Benefits – Hearing exams and hearing aid coverage (with limits).

- Fitness Memberships – Access to gym programs or wellness networks.

- Transportation Services – Non-emergency transportation to medical appointments (availability varies by plan and county).

- Telehealth Services – Virtual doctor visits, increasingly popular among Arizona seniors.

These added benefits can provide both convenience and financial value, particularly for seniors who would otherwise pay out-of-pocket for dental, vision, or hearing care.

How Medicare Advantage Works Differently from Original Medicare

Unlike Original Medicare, which allows you to see any provider nationwide who accepts Medicare, Medicare Advantage plans typically operate within structured provider networks.

Most Arizona plans fall into one of two categories:

- HMO (Health Maintenance Organization):

Requires you to use in-network doctors and hospitals, select a primary care physician (PCP), and obtain referrals for specialists. - PPO (Preferred Provider Organization):

Offers more flexibility, allowing you to see out-of-network providers at a higher cost and usually without referrals.

This network-based structure helps control costs and allows plans to offer additional benefits — but it also means verifying your doctors and hospitals are included before enrolling is essential.

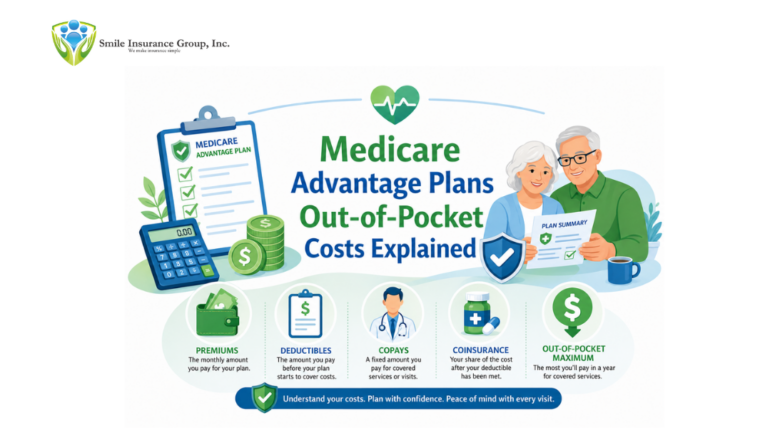

Annual Maximum Out-of-Pocket Protection

A major financial distinction of Medicare Advantage plans is the annual maximum out-of-pocket (MOOP) limit.

Once you reach this spending cap on covered medical services:

- After you reach the annual out-of-pocket limit, the plan covers all eligible medical expenses for the rest of the year.

- You are protected from unlimited medical expenses.

Original Medicare does not have a built-in out-of-pocket maximum unless you purchase a separate Medigap policy. For many Arizona seniors, this built-in protection provides peace of mind, especially when managing chronic conditions or unexpected hospitalizations.

Why This Matters for Arizona Seniors

Arizona has a large and growing Medicare population, and plan availability can vary by county. Urban areas such as Maricopa and Pima counties typically offer more plan options and competitive benefits, while rural counties may have fewer choices.

Understanding how Medicare Advantage works — including costs, networks, and additional benefits — allows seniors to make informed decisions that balance flexibility, affordability, and healthcare access.

Choosing the right plan is not just about monthly premiums. It’s about aligning coverage with your doctors, prescriptions, lifestyle, and long-term financial protection.

Costs of Medicare Advantage Plans in Arizona

The cost of a Medicare Advantage plan in Arizona can vary significantly depending on several key factors:

- County of residence (plan availability and pricing differ by ZIP code)

- Plan type (HMO, PPO, or Special Needs Plan)

- Insurance carrier

- Your healthcare usage and medical needs

Understanding how these variables interact is essential for choosing a cost-effective plan that aligns with your health and financial situation.

1. Monthly Premiums

Many Medicare Advantage plans in Arizona advertise $0 monthly premiums, which makes them attractive at first glance. However, clarifying the implications of this is essential.:

- You must still pay your Medicare Part B premium.

- A $0 premium does not mean $0 healthcare costs.

- Copays, coinsurance, and drug costs still apply.

Some plans charge a higher monthly premium but may offer:

- Lower specialist copays

- Reduced hospital cost-sharing

- Broader provider networks

- Enhanced supplemental benefits

Strategic Insight:

For seniors who see specialists frequently or manage chronic conditions, a slightly higher premium plan with lower copays can reduce total annual costs.

2. Copays & Coinsurance

Instead of paying a percentage (like many traditional insurance plans), Medicare Advantage plans often use fixed copays, making costs more predictable.

Common structures include:

- Primary care visits: Lower fixed copay

- Specialist visits: Higher fixed copay

- Urgent care: Moderate copay

- Hospital stays: Daily copay for the first several days

- Outpatient procedures: Copay or coinsurance depending on service

Drug coverage (when included) also uses tiered pricing:

- Tier 1: Generic drugs (lowest cost)

- Tier 2–5: Brand-name and specialty drugs (higher cost)

Important Consideration:

Review your medication list carefully. A drug placed in a higher tier can significantly impact your annual expenses.

3. Maximum Out-of-Pocket (MOOP)

Every Medicare Advantage plan includes an annual Maximum Out-of-Pocket (MOOP) limit for covered medical services.

Once you reach this limit:

- The plan covers all eligible services for the rest of the calendar year.

- You are protected from unlimited medical spending.

This built-in financial cap is one of Medicare Advantage’s most important protections.

Key Insight (Information Gain)

Many Arizona seniors focus heavily on finding a $0 premium plan but overlook the MOOP. A plan with low premium, high specialist copays, and high MOOP may cost more overall if you require ongoing care or hospitalization.

Instead of comparing premiums alone, evaluate:

- Total annual cost potential

- MOOP limit

- Expected healthcare usage

Looking at total financial exposure provides a clearer picture than monthly cost alone.

Coverage Details: What’s Included?

Medicare Advantage plans must meet federal coverage standards while often offering additional benefits beyond Original Medicare.

Core Coverage

All Medicare Advantage plans are required to cover:

- Inpatient hospital care

- Outpatient medical services

- Preventive screenings (annual wellness visits, cancer screenings, vaccines)

- Emergency and urgent care services

Emergency care is covered nationwide, even if you are outside your home network.

Additional Benefits (Varies by Plan)

Many Arizona Medicare Advantage plans include supplemental benefits not covered by Original Medicare. These may include:

- Dental coverage – Cleanings, exams, X-rays, and sometimes allowances for crowns or dentures

- Vision coverage – Annual eye exams and eyewear allowances

- Hearing benefits – Exams and partial hearing aid coverage

- Over-the-counter (OTC) benefit cards – Allowances for approved health items

- Telehealth services – Virtual primary and specialist visits

- Fitness memberships – Access to wellness and gym programs

- Transportation services – Non-emergency rides to medical appointments (varies by plan)

Unique Insight

Benefit competitiveness often correlates with population density and insurer competition.

- Maricopa County and Pima County typically offer more plan options and richer supplemental benefits.

- Rural counties may have fewer carriers and more limited benefit structures.

This geographic variation makes county-specific plan comparison essential.

Understanding Provider Networks in Arizona

Medicare Advantage plans operate through provider networks. Understanding network structure is critical before enrolling.

HMO (Health Maintenance Organization)

- Must use in-network providers (except emergencies)

- Requires selection of a Primary Care Physician (PCP)

- Referrals required for specialist visits

- Typically lower premiums

- More structured and coordinated care

HMOs can be cost-effective but offer less flexibility.

PPO (Preferred Provider Organization)

- Allows out-of-network visits (higher cost-sharing)

- No referral required for specialists

- Greater provider flexibility

- Often slightly higher premiums

PPO plans may be ideal for seniors who value flexibility or see multiple specialists.

Important Considerations for Arizona Residents

Before enrolling, verify:

- Your preferred hospital system is in-network

- Your primary care physician participates

- Access to needed specialists (cardiology, orthopedics, oncology, etc.)

- Your preferred pharmacy is included in the drug network

Even if a doctor accepts Medicare, they may not accept your specific Medicare Advantage plan.

Snowbird Alert

Many Arizona residents split time between Arizona and another state.

If you:

- Spend summers elsewhere

- Travel frequently

- Maintain residences in multiple states

A PPO plan may offer greater flexibility compared to an HMO, which typically restricts routine care to in-network Arizona providers.

Understanding how your lifestyle affects network access can prevent unexpected out-of-network costs.

By evaluating premiums, copays, MOOP limits, supplemental benefits, and network access together — rather than separately — Arizona seniors can make more informed, financially sound Medicare Advantage decisions.

Comparing Medicare Advantage vs. Original Medicare in Arizona

| Feature | Medicare Advantage | Original Medicare |

| Monthly Premium | Often $0 (plus Part B) | Part B + optional Medigap |

| Drug Coverage | Usually included | Separate Part D required |

| Provider Access | Network-based | Nationwide access |

| Out-of-Pocket Limit | Yes | No cap without Medigap |

| Extra Benefits | Often included | Not included |

Strategic Insight:

Seniors with predictable healthcare needs may benefit from Medicare Advantage’s cost controls. Those who prioritize nationwide provider access may prefer Original Medicare with Medigap.

When Can You Enroll?

Initial Enrollment Period

7-month window around your 65th birthday.

Annual Enrollment Period (Oct 15 – Dec 7)

Switch, enroll, or drop coverage.

Medicare Advantage Open Enrollment (Jan 1 – Mar 31)

Switch to another Advantage plan or return to Original Medicare.

Common Mistakes Arizona Seniors Should Avoid

- Choosing based on premium alone

- Not verifying doctor participation

- Ignoring prescription drug tiers

- Skipping annual plan review

- Overlooking out-of-pocket maximum limits

How to Compare Plans Effectively

To make a confident decision:

- List your current doctors

- List medications and dosages

- Estimate expected healthcare usage

- Compare MOOP limits

- Evaluate plan star ratings

Working with a licensed Medicare advisor can simplify the process and help you avoid costly oversights.

Why Work with Smile Insurance?

Choosing the right Medicare Advantage plan requires local expertise. Smile Insurance helps Arizona seniors:

- Compare multiple carriers

- Evaluate networks and drug formularies

- Understand hidden costs

- Enroll correctly to avoid penalties

Consultations are personalized and designed to match your health needs and budget.

Schedule a free Medicare review with Smile Insurance today to ensure your 2026 coverage is optimized.

FAQ

What is the biggest disadvantage of Medicare Advantage?

Limited provider networks can restrict access to out-of-network doctors.

Are $0 premium Medicare Advantage plans really free?

No, you must still pay your Medicare Part B premium and applicable copays.

Can I keep my doctor with Medicare Advantage in Arizona?

Only if your doctor participates in your plan’s network.

Do Medicare Advantage plans cover prescriptions?

Most plans include Part D prescription drug coverage.

Can I switch plans every year?

Yes, during the Annual Enrollment Period (October 15–December 7).