As Americans reach retirement age, many find themselves at a crossroads when it comes to health insurance. Seniors who are eligible for Medicare often still have access to employer-sponsored health insurance, either through their own job, a spouse’s plan, or retiree coverage. This presents a critical decision: should you keep your employer coverage or switch to a Medicare Supplement (Medigap) plan? At Smile Insurance Group, we understand the complexities of this choice, and we’re here to provide clarity so you can protect both your health and your finances.

Understanding Medicare Supplement Insurance

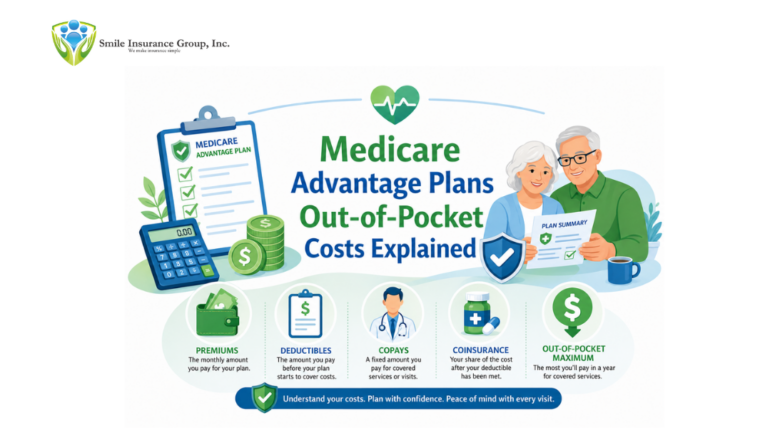

Medicare Supplement, also known as Medigap, is private insurance designed to cover the costs not paid by Original Medicare (Parts A and B). These costs include:

- Deductibles

- Copayments

- Coinsurance

Medigap policies are standardized and labeled by letters (Plan A, B, C, D, F, G, K, L, M, and N), each offering a different level of coverage. For example:

- Plan G: Covers nearly all out-of-pocket expenses except the Part B deductible.

- Plan N: Offers lower premiums but requires small copays for doctor and ER visits.

The key advantage of Medicare Supplement is financial predictability. Beneficiaries know their premiums upfront and enjoy minimal unexpected costs when seeking medical care.

What Employer Coverage Provides

Employer coverage is group health insurance offered to employees, retirees, or dependents. It typically includes:

- Hospital and medical care (similar to Medicare Parts A and B)

- Prescription drug coverage (which may eliminate the need for Part D)

- Additional benefits such as dental, vision, and hearing care

- Family coverage options if dependents need insurance

Employer-sponsored plans often share costs between the employer and employee, with the employer paying a significant portion of premiums. This can make employer coverage more affordable for some seniors, depending on how much their company contributes.

Key Factors to Consider When Choosing Between Medicare Supplement vs. Employer Coverage

When deciding between these two options, consider the following factors in detail:

1. Cost of Premiums

- Medicare Supplement: Premiums vary by plan type, age, and location. Although you may pay higher monthly premiums, Medigap often results in lower out-of-pocket expenses during care.

- Employer Coverage: Premiums depend on how much your employer subsidizes. Some retirees enjoy low-cost or even premium-free coverage. Others may find employer coverage more expensive than Medigap.

2. Out-of-Pocket Expenses

- Medicare Supplement: Provides predictable costs with little to no surprise medical bills. Plan G and Plan F (for those eligible) cover nearly everything except the Part B deductible.

- Employer Coverage: May involve higher copayments, deductibles, or coinsurance depending on the employer plan’s structure.

3. Prescription Drug Coverage

- Medicare Supplement: Does not include prescription drug coverage. You would need to purchase a Medicare Part D plan separately.

- Employer Coverage: Often includes prescription coverage, which may eliminate the need for Part D.

4. Provider Networks

- Medicare Supplement: Works with any provider that accepts Medicare nationwide, offering maximum flexibility.

- Employer Coverage: May restrict you to a network of doctors and hospitals, especially if it’s an HMO or PPO.

5. Coverage for Dependents

- Medicare Supplement: Only covers the individual. Each spouse would need their own Medicare Supplement plan.

- Employer Coverage: May allow you to cover your spouse or dependents under the same plan, making it more cost-effective for families.

6. Portability of Coverage

- Medicare Supplement: Coverage follows you anywhere in the United States. Some plans even offer limited international coverage.

- Employer Coverage: Coverage may end if you leave employment or if the employer discontinues retiree benefits.

When Medicare Supplement Makes More Sense

- If your employer does not subsidize retiree coverage and premiums are high.

- If you want freedom to see any doctor or specialist nationwide without network restrictions.

- If you travel frequently or live in multiple states throughout the year.

- If you prefer predictable healthcare expenses with minimal out-of-pocket surprises.

When Employer Coverage Is the Better Choice

- If your employer subsidizes a large portion of your premium, making it much cheaper than Medigap.

- If your employer plan includes robust prescription drug coverage, dental, vision, or hearing care.

- If you want to keep dependents covered under the same plan.

- If your employer offers retiree benefits that match or exceed what Medicare provides.

Common Mistakes to Avoid

Making the wrong choice can result in unnecessary expenses or gaps in coverage. Avoid these mistakes:

- Delaying enrollment in Medicare Part B: If you keep employer coverage, confirm it’s considered “creditable coverage.” Otherwise, you may face penalties when enrolling later.

- Not comparing total costs: Premiums are only part of the equation. Consider deductibles, copays, and coinsurance.

- Assuming employer coverage lasts forever: Some companies discontinue retiree benefits, leaving seniors scrambling for coverage.

- Overlooking drug coverage: If your employer plan doesn’t provide adequate drug benefits, you may need Part D to avoid penalties.

How to Transition from Employer Coverage to Medicare Supplement

If you decide to switch, follow these steps carefully:

- Confirm End of Employer Coverage: Check with your HR or benefits department to determine when your coverage ends.

- Enroll in Medicare Part B: You’ll need both Part A and Part B to qualify for Medicare Supplement.

- Apply for a Medigap Plan: The best time is during your Medigap Open Enrollment Period, which lasts six months after you enroll in Part B. During this period, you cannot be denied coverage or charged more due to health conditions.

- Add Part D Coverage: Choose a prescription drug plan if you don’t have creditable coverage through your employer.

Proper timing ensures you avoid gaps in insurance and penalties.

Balancing Costs and Benefits for Your Future

The choice between Medicare Supplement and employer coverage is not one-size-fits-all. It depends on your health needs, financial situation, and whether you need family coverage. Carefully compare both options and project your long-term healthcare costs. While employer coverage may look cheaper upfront, Medigap can provide greater stability and peace of mind in the long run.

Conclusion: Choose the Right Coverage with Expert Guidance

Choosing between Medicare Supplement and employer coverage is one of the most important healthcare decisions seniors face. The right choice can save thousands of dollars and ensure access to the care you need without financial strain.

At Smile Insurance Group, we specialize in helping seniors evaluate their unique situations. Our team will compare your employer plan with available Medigap options, break down the costs, and guide you toward the coverage that gives you the best value and security.

Contact Smile Insurance Group today to make the smart choice for your healthcare future. Protect your health, your wallet, and your peace of mind with expert guidance.